Financial To-Do’s When Starting A New Job

Blog post

09/01/22Starting a new job and/or switching careers can be a financial stressor in people’s lives. Outlined below are some of the most important financial to-do’s when starting a new job:

Enroll in new employer sponsored retirement plans

1. Savings strategy

Your first step in enrolling in a new retirement plan is to assess your current savings strategy. Are you saving enough? Are you saving to the right types of accounts? Are you achieving your financial goals, now and in retirement? Is there an employer match you should be taking advantage of? If you do not know the answer to those questions or if they make you second guess your savings strategy, consider reading THOR’s previous blogs on savings.

2. Choosing investment options

Your plan may offer various mutual funds and target-date funds, but rarely individual stocks or bonds. If you are young and have a long time until retirement, you should avoid choosing fixed income and bond funds. Investing more aggressively will allow you to accumulate more assets in your account. As you approach retirement, you should begin to add these options. If you want to take a more simplified approach, consider choosing a target-date fund associated with your projected retirement date. For a complete understanding of target-date funds, read THOR’s previous blog titled: Target Date Funds: 401k’s most popular investment choice. If you currently use a financial advisor, ask them for assistance in choosing your investment options.

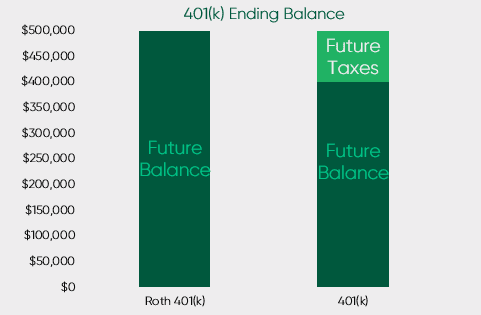

3. Roth 401(k) vs. Pre-Tax 401(k)

Once you have chosen your investment options, you need to decide whether your contributions should be made on a pre-tax, after-tax, or a combination of the two. Pre-tax contributions are deposited into your account before tax is paid on them. They grow on a tax-deferred basis. When you start taking distributions after age 59 ½, you pay income tax on the withdrawals.

When you make Roth 401(k) contributions, the funds enter your account after you have paid tax on them. They grow-tax free and any distributions you take after age 59 ½ are tax-free. Depending on your situation, it may be advantageous to begin saving Roth dollars at an early age. Doing so provides for an extended period of tax-free growth.

4. Beneficiaries

Naming beneficiaries for your retirement accounts is a crucial step and is often missed. Make sure you name beneficiaries for all your retirement accounts. It is important to add both primary and contingent beneficiaries.

- A primary beneficiary is the person who receives your assets upon your death. For employer sponsored retirement plans, federal law requires you to name your spouse as your primary beneficiary unless he or she waives that right.

- A contingent beneficiary is the person who receives your assets in the event your primary beneficiary predeceases you. If you have children, you will typically name them.

- Beneficiary designations prevail over a will.

Previous employer sponsored retirement plans

If you have a retirement account with your previous employer, you will need to decide what to do with it. You have a few options with the old retirement plan since you no longer are contributing to it.

Maintain two accounts

Your first option is to keep your old account open. If this option interests you, you will have to check with your previous employer to see if they allow you to do this as some employers prohibit it. In most cases, this is the least beneficial option. The downside is that the account is often forgotten when reviewing your other accounts and you are limited to the mix of investment options provided in the plan. You may also be subject to maintenance fees.

401(k) Rollover

The second option is to roll the funds from your old retirement account into your new retirement account. With this option, you will still be limited to the number of investment options available to you under the new plan, but if you do not currently work with an investment advisor, it can be the simplest option. There are no tax consequences when making this transfer.

IRA rollover

Your third option is to roll your old 401(k) balance into an IRA (individual retirement account). There are no tax consequences when choosing this option. The main benefit of this option is the greater number of investment options available in an IRA. This will allow you or your investment advisor to create a more customized portfolio. With an IRA, you can now execute Roth conversions. Roth conversions allow you to transfer traditional IRA funds to a Roth IRA, pay tax on the value of the assets transferred and have the funds in the Roth IRA grow tax-free and be distributed tax-free. The downside of doing an IRA rollover is that it can eliminate the ability to use the back door Roth strategy. For more information on the Back Door Roth strategy read our blog that goes into more details.

Health Care

When choosing a health care plan, you should consider your family’s health and what kind of care you need.

Compare Old and New Coverage

The first step is comparing your old coverage with your new coverage. If your old plan is better than your new plan, or if your new employer does not offer health coverage, consider staying on your old plan by signing up for COBRA coverage. You should also review your spouse’s health care benefits and marketplace coverage to ensure you are getting the best coverage.

High-Deductible Health Care Plan & Health Savings Account

If you are healthy and have low medical expenses, consider enrolling in a high deductible health care plan if your employer offers one. A high deductible health care plan offers lower premiums with a higher deductible. This is the only type of plan that allows you to contribute to a health savings account (HSA). The benefit of an HSA is threefold. Contributions go into the account pre-tax, funds grow tax-free, and when the funds are used for medical expenses, they are distributed tax-free. If you have an HSA account from your previous employer, you can consolidate the accounts to your new employer’s HSA. If you would like to read more about the benefits of an HSA, refer to our last blog about HSAs.

Flexible Savings Account (FSA)

Flexible Savings Accounts are on a “use it” or “lose it” basis. Meaning, if you plan to leave your employer, you should begin submitting claims to have your out-of-pocket medical expenses reimbursed.

Disability & Life Insurance

When changing employers, it is important to evaluate your current disability and life insurance coverage. There are several questions you should ask yourself about life and disability insurance – What coverage will I be losing? What does my new company offer? Do I need additional coverage outside of my employer? You should also remember the following:

- Do not forget to name beneficiaries.

- Consider policies outside of your employer. If you leave your job and need to purchase new life insurance, you will have to redo the underwriting process. That process could result in your new policy being more expensive, or it could result in a denial of coverage.

Updating your financial plan

You should never make financial decisions without understanding your financial situation. Maybe the strategy you are trying to implement does not make sense to you. A financial plan can assist you in developing a savings strategy, establishing/adjusting a budget, setting big financial goals, optimizing tax savings, determining a retirement age, and more. When starting a new job, you should update your financial plan to ensure you are still on track to meet your goals.

We hope this blog helps you if you are considering or have recently started a new job. If you have questions about any of these items, consider reaching out to a financial advisor.