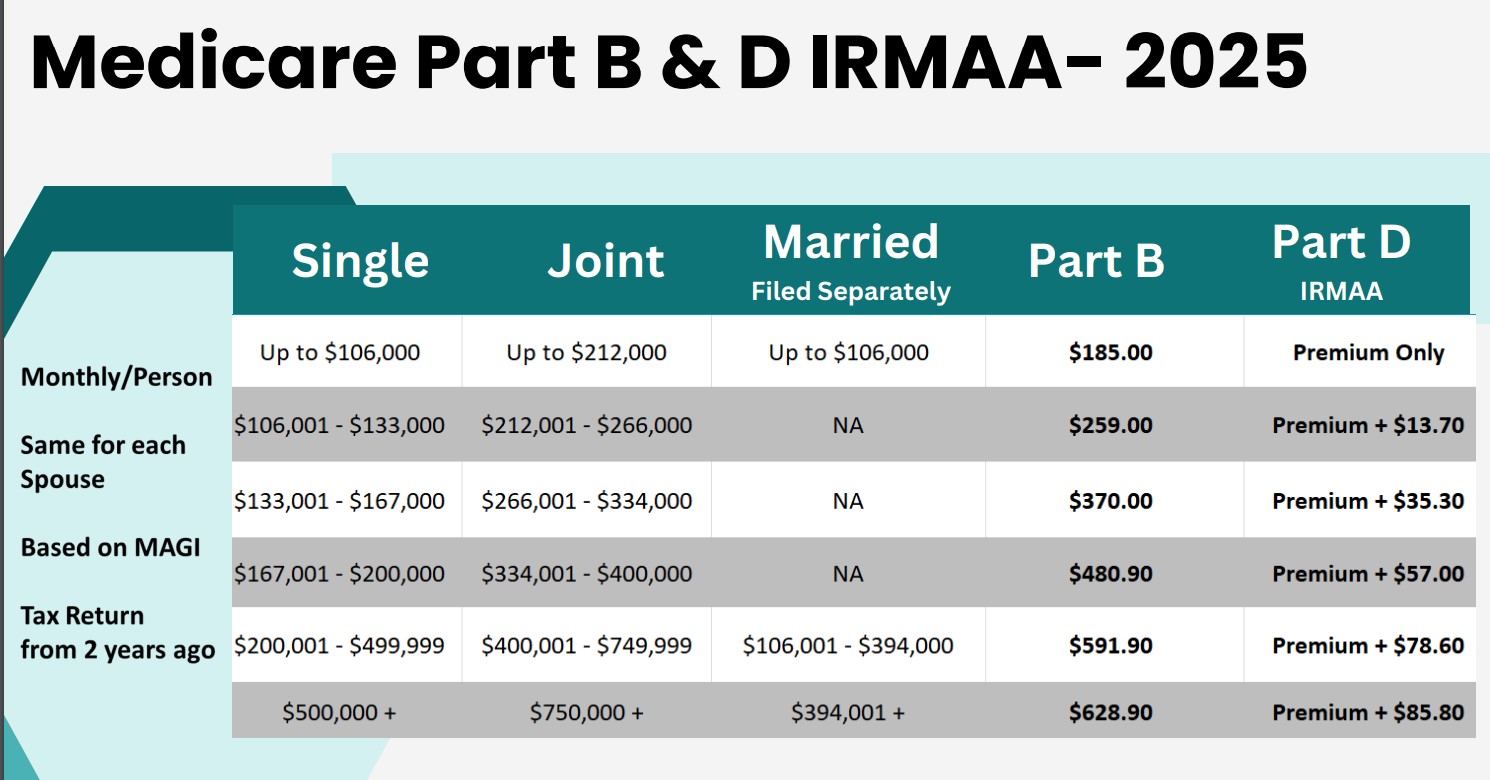

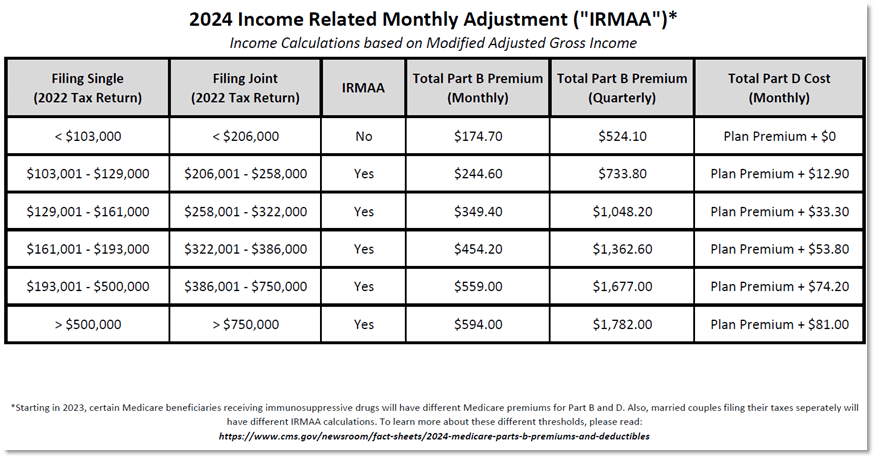

As most people know, Medicare eligibility begins at age 65. And once you are enrolled in Medicare, your premiums are determined based on your level of income (the idea being that those with higher income pay higher premiums). But here is the catch – it is not your most recent tax year that determines your premiums. Rather, Medicare looks back two tax years (often referred to as “prior prior”). This means that if you are going on Medicare in 2024, your premiums would be based on your income from your 2022 tax return. This nuance within Medicare is what I wanted to write this blog about because it is both lesser-known and often overlooked.

Medicare’s two-year lookback

Often, Medicare’s two-year lookback can capture a year that looks quite different than the taxpayer’s current situation. A common example would be that you were working at age 63, earning a full wage, and then retired the following year, at age 64 – halting all earned income. In this example, Medicare would determine your soon-to-be premium based on your age 63 wages – which have since ended. If you took no intervention, you could be signing up (by default) to pay for higher premiums than what is necessary!

Where Form SSA-44 comes into play

Luckily, Medicare provides a way to request a change in what would otherwise be your premium amount. Completing Form SSA-44 allows the taxpayer to specify why they are a candidate for a lower premium amount. Medicare provides a list of “life-changing events” that would qualify you for a lower premium. These include events like work stoppage or reduction, marriage, divorce, death of a spouse, loss of income-producing property, loss of pension income, or employer settlement payments.

Conclusion

Unlike trickling into a higher tax bracket, where just the last few dollars you make slide into the higher tax rate, Medicare’s Income Related Monthly Adjustment Amounts (IRMAA) are a cliff – aka $1 over the limit equals the higher premium amount. This can equate to thousands of dollars in added premiums in some situations!

If you have questions and would like to talk with us further, please call us at 513-271-6777. For more THOR reading, click here to go to the Blogs and Market Updates section on our website. Follow us on social media:

{kind=link}

{kind=link}